I pulled ECB BSI credit data and Eurostat nominal GDP figures to reconstruct credit-to-GDP ratios for five major European economies over a fourteen-year period.

The goal was to assess how private sector leverage actually evolved after the global financial crisis.

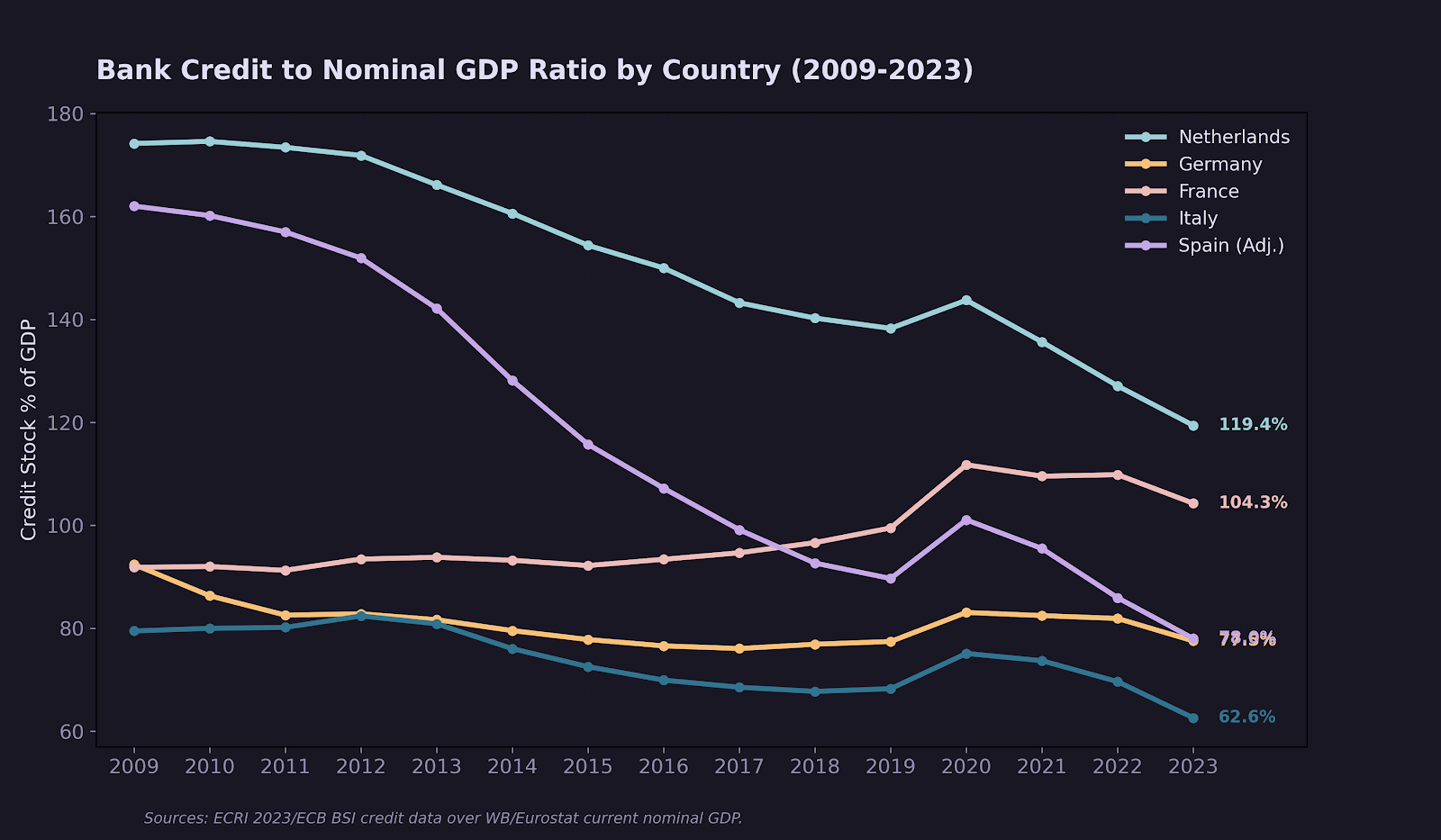

For Spain, I adjusted the credit stock to account for off-balance-sheet securitization that was active before 2009 and would otherwise understate peak leverage.

The data shows five countries with a common monetary policy and substantially different credit trajectories.

France is the only large economy in this sample where the credit-to-GDP ratio increased from start to finish – from 92% in 2009 to 104.3% in 2023. Credit growth has persistently exceeded nominal output growth.

Germany held near-flat ratios throughout the period. Nominal credit growth and nominal GDP growth moved together, keeping leverage around 77–79%. There was no credit boom and no contraction.

Spain's adjusted figure shows a peak near 162% of GDP. By 2023 the ratio stood at 78.9%, with one of the largest private sector deleveraging episodes in modern European history.

Italy ends at 62.6%, the lowest ratio in this group. The decline reflects a decade of credit stagnation, a persistent non-performing loan problem, and weak nominal expansion. Low leverage in this context is a symptom and not a sign of financial health.

The Netherlands maintained structurally high ratios throughout, supported by fiscal incentives for mortgage debt, declining from above 175% to 119.4%.

The ECB sets one interest rate for all five of these economies.

The transmission of that rate through the banking system differs materially across them. An asymmetry that is a core problem for European monetary policy.

by RagionamentiFinanza

2 Comments

crazy how Spain went from 162% to like 79%

Less and less activity worth supporting with credit… not good