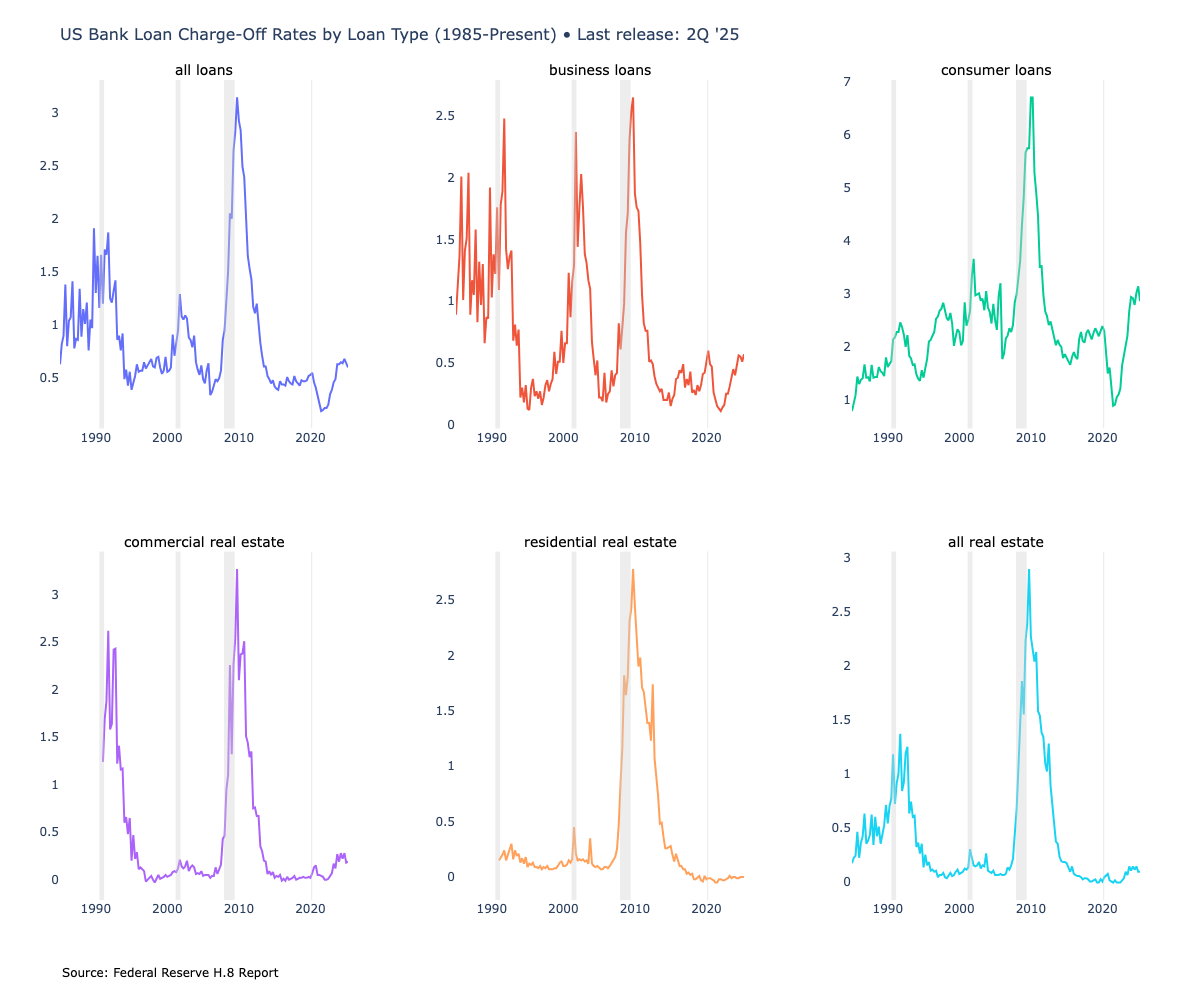

This visualization shows US bank loan charge-off rates by loan type from 1985 to present, using Federal Reserve H.8 data. Charge-offs represent loans that banks have given up trying to collect—essentially their admission that the money is gone forever.

The savings and loan crisis in the 1990s was centered around commercial real estate and business loans that couldn’t handle the Volcker rate hikes into double digits. 2001 was centered on the pop in the tech bubble and the over investment in telecom space. 2008 started as a residential real estate crisis that then led to mass unemployment and consumer weakness. So far, the only noticeable issue is a tick up in consumer loans, though more a normalization from post covid lows than anything else.

The major caveat to this analysis is that H.8 data only covers commercial banks, not the broader financial system. Fintechs and private credit lenders are not part of this dataset.

by DataVizHonduran

4 Comments

Source: Federal Reserve data [https://www.federalreserve.gov/releases/chargeoff/chgallsa.htm](https://www.federalreserve.gov/releases/chargeoff/chgallsa.htm) Tools: python and plotly

I’d like to see the same data points for loan originations of various types over time.

>The savings and loan crisis in the 1990s was centered around commercial real estate and business loans that couldn’t handle the Volcker rate hikes into double digits.

The S&L crisis was more of an 80s thing, as rates peaked in ‘81, and during the early to mid-80s, interest rate cap regulations were removed. Banks had to compete on deposit rates, which meant their funding costs zoomed upward.

That was the best case, though. A new invention (money market funds / accounts!) were already sucking money out of the banking system because they offered way better rates.

It’s not that dissimilar from what we saw in ‘22 and ‘23. After a period of relatively low rates, the Fed taking short term rates above 5% enticed people to move money that sat in lower yielding accounts into higher yielding accounts. Obviously the magnitude of rate changes was a lot smaller, but it’s also a lot easier to change banks these days.

What about the large amount of underwater treasurys that the Fed is letting banks hold onto? You do add one small caveat, but you forget to mention that PE has steeped in a lot lately. PE acting as banks is the concern. Pretty misleading title.